Buying a Home: What to Know Before You Get the Keys

Buying a home is exciting. Most people picture the fun parts first: finding the perfect place, placing the couch, or watching a dog run around the backyard.

What’s often harder is figuring out how to make that dream a reality.

From understanding what you can afford to choosing the right mortgage and avoiding costly mistakes, the home buying process can feel overwhelming. The good news? With the right guidance, it doesn’t have to be.

Here’s a straightforward breakdown of what to expect, so you can feel confident and prepared as you unlock the door to homeownership.

Start With a Mortgage Expert (Mortgage Loan Officer)

For most buyers, a mortgage (or home loan) makes buying a house possible. A mortgage expert acts as your financial guide throughout the process and can help you:

- Understand how much home you can realistically afford

- Compare mortgage options

- Navigate the loan process, from pre-approval to closing

You’re not expected to know everything. That’s what your Ascentra Mortgage Expert is there for.

Shopping for the Right Home

Finding the right home can be challenging, but it’s important to be realistic. Make a list of must-haves, identify dealbreakers, and stay open to compromise. If you’re considering a fixer-upper, be honest with yourself about your skills, budget, and time.

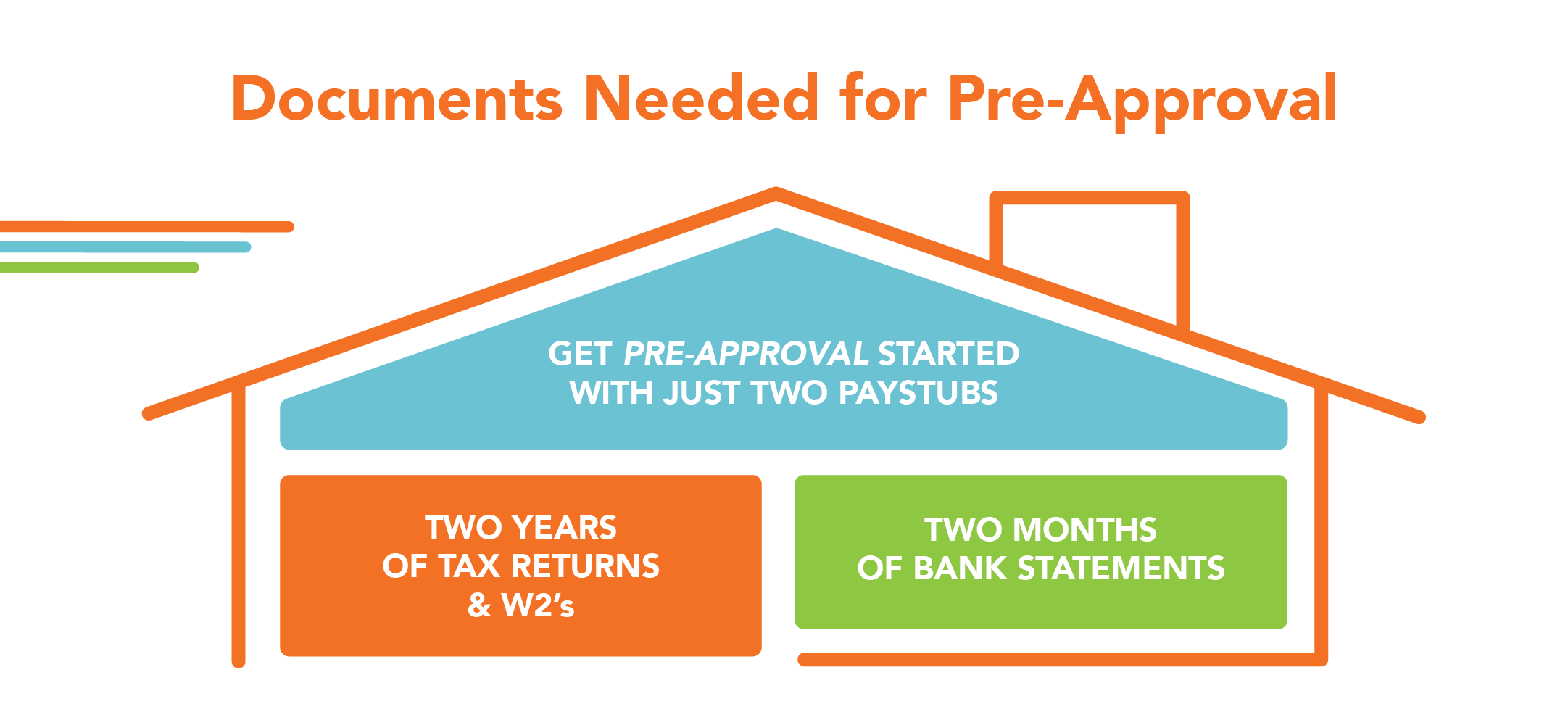

Pre-qualification vs. Pre-approval

Pre-qualification is a rough estimate based on basic information. Pre-approval verifies your income and finances by reviewing official documents.

- Often required by realtors

- Show sellers you’re a serious buyer

Neither guarantees final loan approval; further verification happens after you make an offer. Ascentra only offers pre-approvals.

GET PRE-APPROVED

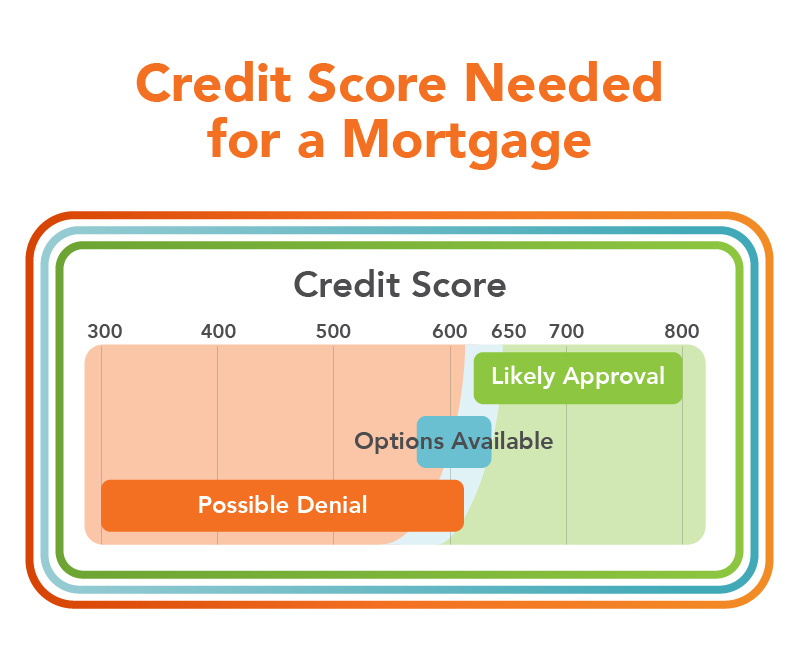

Lenders also consider a borrower’s credit score and employment history.

While a score of 620 is preferred, approval is based on multiple factors, including stable, consistent income with no unexplained gaps or reductions. At Ascentra, qualified borrowers receive the best available rate on traditional fixed-rate mortgages, without rate increases tied solely to credit score.

No matter where you are on your homebuying journey, Ascentra is here to help. Mortgage options may be available for borrowers with lower credit scores, and our financial coaches can help you build a stronger financial foundation for the future.

Common Mortgage Options

Choosing the right mortgage plays a key role in long-term affordability.

- Fixed-rate mortgages remain the most common option, offering stable payments over 10, 15, or 30 years.

- Adjustable-rate mortgages (ARM) may offer lower initial rates for a set period, though payments can change later based on the economy.

An ARM can be beneficial when interest rates are high and expected to drop, but payments may increase if rates rise.

Down Payment

One of the biggest hurdles for first‑time buyers is the upfront cost. Down payments typically range from 3 to 5% of a home’s purchase price, and buyers may also need to cover closing costs. For those struggling to save while managing rent, student loans, and daily expenses, those costs can feel out of reach.

Closing Costs

Closing costs are fees required to finalize the mortgage. They may include additional fees for appraisals, inspections, and title services, and attorney and loan processing fees. These typically add an additional 2 – 6% to the home’s purchase price.

Note: In some cases, buyers can negotiate for the seller to cover part or all of these costs during the offer process.

How Much Can You Afford?

A good starting point is running the numbers yourself. Use our calculator below to estimate your monthly payment, then connect with a mortgage expert for a full picture — including the insurance, property tax, and closing cost fees that make up your true total.

SEE WHAT YOU CAN AFFORD

What Is Private Mortgage Insurance (PMI)?

When configuring your loan and working with your mortgage expert, it’s important to know that if your down payment is less than 20% of the total home value, you’ll be required to pay for PMI.

PMI protects the lender if the loan goes into foreclosure, not the borrower. In many cases, PMI can be removed once the borrower has built 20% equity in the home, though some exceptions may apply.

Down Payment Assistance & Grants

If saving for a down payment feels challenging, assistance programs may help. Some cities, counties, and organizations offer grants for income‑eligible buyers and/or homes purchased in certain locations.

To help make homeownership more attainable, Ascentra offers a $15,000 First‑Time Home Buyers Grant for income‑qualified buyers through a partnership with the Federal Home Loan Bank of Des Moines. These grants are subject to funding availability and can be used toward both down payment and closing costs, helping to reduce the upfront financial burden.

Ongoing Costs of Homeownership

Now that you’ve found your house, worked through the loan options and understand the additional fees, it’s time to think about the ongoing costs of homeownership.

Homeowners Insurance

Home insurance helps protect you from fire, severe weather, theft or burglary, or other unexpected losses. These coverages and cost vary by provider, so research and plan according to your specific needs and wants.

Property Taxes

Property taxes are assessed by the county and depend on home location and property value and features.

Both insurance and property taxes can be paid separately or rolled into your monthly mortgage payment. Note: these costs often rise over time, which can increase your monthly payment.

Repairs and Emergencies

Homeownership also brings responsibility for repairs and maintenance. Plumbing issues, roof leaks and appliance breakdowns are no longer a landlord’s responsibility. Financial experts often recommend setting aside savings equal to about three months of mortgage payments to help cover unexpected repairs or rising costs.

A Critical Tip: Don’t Make Financial Changes

Once buyers apply for a mortgage, financial stability is critical. Opening new credit cards, making large purchases or moving significant amounts of money can put loan approval at risk.

ITIN Lending Option

Borrowers without a Social Security number may qualify for ITIN lending.

The IRS issues an Individual Taxpayer Identification Number (ITIN), which can be used to apply for a mortgage at participating banks or credit unions, including Ascentra.

From Offer to Closing

After your offer is accepted, your mortgage officer helps manage your appraisals, title work, and flood certifications.

During this time, you’ll shop for homeowner’s insurance and may continue negotiations with the sellers after the new house has been inspected.

From choosing your new home to its closing day, the process typically takes 30 to 45 days. At closing, final documents are signed, remaining payments are made and keys are transferred, usually within one to two hours.

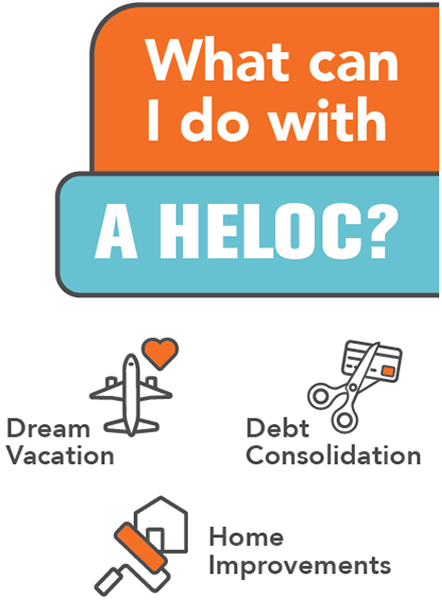

A Smarter Way to Borrow for Homeowners

During the early-to-mid stages of homeownership, many homeowners begin to accumulate equity in their homes. That equity isn’t just a number on paper; it can be a powerful financial tool. One of the most flexible ways to access it is through a Home Equity Line of Credit or HELOC from Ascentra Credit Union.

A HELOC works like a credit card backed by the value of your home. Instead of taking out a lump sum loan, you are approved for a credit limit, and you can borrow what you need when you need it. Interest is charged only on the amount you actually use, making it a more cost-effective and flexible option than many other types of borrowing.

So, why is a HELOC a better way to borrow money?

- Interest rates are typically lower than credit cards, personal loans, or even some auto loans because your home acts as collateral. This means a lower monthly payment and less interest over time.

- Repayment terms are flexible. During the draw period, usually 5 – 10 years, you can make interest-only payments or pay down the principal as your budget allows. Afterwards, you enter the repayment period, giving you predictable monthly payments over the remaining term.

- HELOCs are also ideal for specific life goals that many people face: home renovations, debt consolidation, education expenses or major family milestones. Unlike personal loans, which are fixed and can limit your options, a HELOC gives you access to funds whenever you need them, with the ability to borrow multiple times within your credit limit.

It’s important to borrow wisely but for those who plan wisely, a HELOC can provide financial flexibility, lower costs and peace of mind that comes with knowing you’re borrowing smartly. Ascentra is here to help. Before taking out your next loan, consider if a HELOC is a better way to borrow the money needed. Reach out to one of our dedicated Home Equity Specialists to learn how a HELOC may be a better way for you to borrow. Get started at ascentra.org/heloc.