Making Cents of Your Credit Score

Did you know that your credit score could be quietly draining your wallet without you even realizing it?

Whether you’re applying for a loan, renting an apartment, or shopping for car insurance, your credit score plays a significant role in your financial future. Understanding how it works can empower you to take control and save a substantial amount of money.

In this article, we will break down what your credit score consists of, what factors can negatively impact it, how to improve it, and why it matters more than you might think.

Your credit score is calculated based on five main factors:

- Payment History (40%) - This is the most important factor, tracking whether you pay your bills on time. Just one missed payment can take up to two years to recover from. Even after paying off a debt, it may remain on your report for 7–10 years.

- Credit Usage (23%) - Also known as credit utilization, this measures how much of your available credit you're using. Experts recommend keeping your utilization under 30%.

- Credit Age (21%) - This refers to the average age of your open accounts. Closing long-standing credit lines or opening too many new accounts can reduce this average and negatively affect your score.

- Mix of Credit (11%) - Lenders prefer to see a variety of credit types, including installment loans (like mortgages or car loans) and revolving credit (like credit cards). A healthy mix can boost your score.

- Hard Inquiries (5%) - Each time you apply for credit (credit cards, loans, etc.), a hard inquiry is made, which can negatively impact your score, even if you’re not approved. Soft inquiries, like those made by landlords or employers, do not affect your score.

When you understand what makes up your credit score, you can start building or repairing your credit.

If you’re just starting, consider applying for a low-interest credit card from Ascentra Credit Union. Use it for small purchases and pay it off each month to establish consistent, positive history and avoid interest charges.

Free financial coaching is available to help you through the process. At Ascentra Credit Union, we offer coaching services at eight branch locations, including Spanish-speaking support. Our coaches review your credit with a soft inquiry, ensuring it doesn’t affect your score, and create a personalized action plan to assist you with budgeting, debt reduction, and long-term planning.

Online services like SavvyMoney, available through Ascentra’s Digital Banking, let you view your credit report and receive tips on how to improve it. Avoid apps that sell your data; stick to trusted sources like AnnualCreditReport.com, where you can obtain a free report from TransUnion, Equifax, and Experian once a year.

You may also want to consider a consolidation loan that combines multiple debts into one lower-interest payment, which can help with your payment history, credit usage and credit mix. Just be careful not to use the paid-off credit lines and don’t close them, as doing so could hurt your score.

Taking these steps is a fantastic start to building or repairing your credit. You may begin to see positive changes on your credit report within a month.

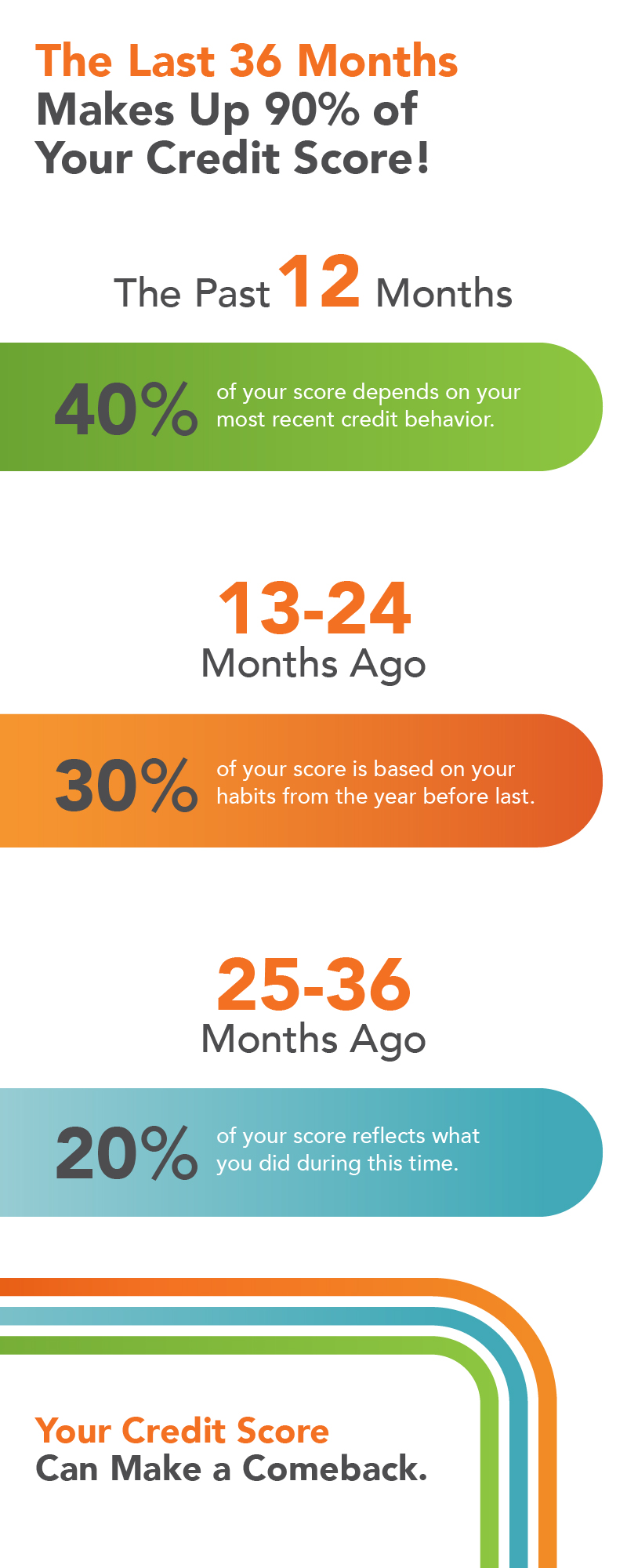

Most of your credit score (90%) is based on activity from the past three years:

- 40% from the last 12 months

- 30% from the previous 13–24 months

- 20% from the previous 25–36 months

So, although there is no instant fix, progress is certainly achievable with time and effort.

Your credit score doesn’t just determine whether you get approved for a loan; it also impacts how much you’ll pay.

- A higher credit score could save you tens of thousands of dollars on a mortgage.

- Lower scores can double your car insurance premiums.

- Employers sometimes run soft credit checks during hiring, and poor credit might limit job offers.

However, keep in mind that your income, rent payments or how long you’ve been employed do not affect your credit score. While they may influence loan decisions, they are not factored into the score itself!

Improving your credit score isn’t about achieving perfection but about making consistent progress.

You can do this by focusing on your payment history, credit usage, credit age, mix of credit, and hard inquiries. If you’re unsure where to start, ask for help! Ascentra Credit Union is here to support you with coaching, tools, and guidance tailored to your specific goals.

Your credit journey is just that, a journey.

Take the first step today and keep moving forward.

×

×

×

A Smarter Way to Borrow for Homeowners

During the early-to-mid stages of homeownership, many homeowners begin to accumulate equity in their homes. That equity isn’t just a number on paper; it can be a powerful financial tool. One of the most flexible ways to access it is through a Home Equity Line of Credit or HELOC from Ascentra Credit Union.

A HELOC works like a credit card backed by the value of your home. Instead of taking out a lump sum loan, you are approved for a credit limit, and you can borrow what you need when you need it. Interest is charged only on the amount you actually use, making it a more cost-effective and flexible option than many other types of borrowing.

So, why is a HELOC a better way to borrow money?

- Interest rates are typically lower than credit cards, personal loans, or even some auto loans because your home acts as collateral. This means a lower monthly payment and less interest over time.

- Repayment terms are flexible. During the draw period, usually 5 – 10 years, you can make interest-only payments or pay down the principal as your budget allows. Afterwards, you enter the repayment period, giving you predictable monthly payments over the remaining term.

- HELOCs are also ideal for specific life goals that many people face: home renovations, debt consolidation, education expenses or major family milestones. Unlike personal loans, which are fixed and can limit your options, a HELOC gives you access to funds whenever you need them, with the ability to borrow multiple times within your credit limit.

It’s important to borrow wisely but for those who plan wisely, a HELOC can provide financial flexibility, lower costs and peace of mind that comes with knowing you’re borrowing smartly. Ascentra is here to help. Before taking out your next loan, consider if a HELOC is a better way to borrow the money needed. Reach out to one of our dedicated Home Equity Specialists to learn how a HELOC may be a better way for you to borrow. Get started at ascentra.org/heloc.