What Sets Credit Unions Apart?

Credit unions offer a community-focused, member-owned alternative to traditional banking services. Unlike for-profit banks, which prioritize shareholder profits, credit unions serve the needs of their members. This fundamental difference influences all aspects of credit union operations, including the products they provide and the values they promote.

Additionally, credit unions are closely connected to local communities. This enables them to deliver personalized service and a strong commitment to financial education that goes beyond simple transactions. Many credit unions enhance financial wellness by providing free workshops, counseling, and youth savings programs.

Discover why credit unions are not only different but also make a positive impact by exploring the following resources.

The Difference Between Credit Unions and Banks

Credit Unions

- Ownership: Member-owned; each member is a part-owner.

- Income Model: Not-for-profit; earnings returned to members via better rates and lower fees.

- Governance: Democratically controlled; one member, one vote.

- Focus: Focused on members' needs, not shareholders.

- Rates & Fees: Offer higher savings rates, lower loan rates and fewer/lower fees.

- Community Involvement: Often community-based and mission-driven.

- Service Approach: Personalized, relationship-based service.

- Eligibility: Must meet membership requirements (location).

Traditional Banks

- Ownership: Shareholder-owned; focused on maximizing investor returns.

- Income Model: For-profit; profits go to shareholders.

- Governance: Controlled by a board elected by shareholders.

- Focus: Prioritizes profit over customer needs.

- Rates & Fees: Often lower savings rates, higher loan rates and more fees.

- Community Involvement: Less locally focused; community involvement varies.

- Service Approach: Standardized service; may be less personal.

- Eligibility: Open to the general public with no membership restrictions.

The Ascentra Difference

What Sets Ascentra Apart?

Unlike banks, we don’t answer to stockholders or investors, we answer to YOU. As a local, democratically controlled not-for-profit, each member of Ascentra Credit Union owns a share in the credit union. When you join Ascentra, you are not a customer you're a member-owner and are treated as such.

We put people before profits. Those profits then go back to you, in the form of lower interest rates on loans, higher returns on your deposits, and lower fees.

For our 40,000 members who directly benefit from our cooperative model, it's more than just about financial services, it’s about being part of an organization made up of people who genuinely care about your financial well-being and the communities we serve. An organization that is always listening, caring, and doing what’s right.

Ascentra Scholarship Program

Each year, Ascentra offers up to $15,000 in scholarships to assist student members planning to further their education through undergrad programs, continuing education (post graduate) or through trades/vocational programs.

Applications open in October and close in March of each year.

LEARN MORE

Ascentra Foundation

The mission of the Ascentra Credit Union Foundation is to improve the quality of life for the membership of Ascentra Credit Union and further the philanthropic outreach in the communities we serve.

$1,035,092

in local charitable

contributions since 2015

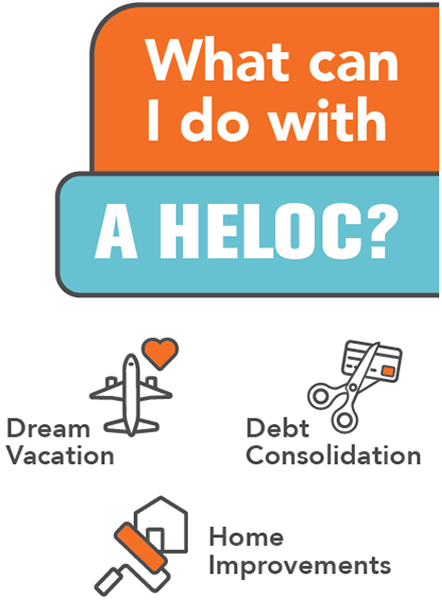

A Smarter Way to Borrow for Homeowners

During the early-to-mid stages of homeownership, many homeowners begin to accumulate equity in their homes. That equity isn’t just a number on paper; it can be a powerful financial tool. One of the most flexible ways to access it is through a Home Equity Line of Credit or HELOC from Ascentra Credit Union.

A HELOC works like a credit card backed by the value of your home. Instead of taking out a lump sum loan, you are approved for a credit limit, and you can borrow what you need when you need it. Interest is charged only on the amount you actually use, making it a more cost-effective and flexible option than many other types of borrowing.

So, why is a HELOC a better way to borrow money?

- Interest rates are typically lower than credit cards, personal loans, or even some auto loans because your home acts as collateral. This means a lower monthly payment and less interest over time.

- Repayment terms are flexible. During the draw period, usually 5 – 10 years, you can make interest-only payments or pay down the principal as your budget allows. Afterwards, you enter the repayment period, giving you predictable monthly payments over the remaining term.

- HELOCs are also ideal for specific life goals that many people face: home renovations, debt consolidation, education expenses or major family milestones. Unlike personal loans, which are fixed and can limit your options, a HELOC gives you access to funds whenever you need them, with the ability to borrow multiple times within your credit limit.

It’s important to borrow wisely but for those who plan wisely, a HELOC can provide financial flexibility, lower costs and peace of mind that comes with knowing you’re borrowing smartly. Ascentra is here to help. Before taking out your next loan, consider if a HELOC is a better way to borrow the money needed. Reach out to one of our dedicated Home Equity Specialists to learn how a HELOC may be a better way for you to borrow. Get started at ascentra.org/heloc.