Thinking Beyond the Test Drive

Buying a vehicle is one of the biggest financial decisions many people make, especially if it is your first time. Understanding the full cost of vehicle ownership can help prevent costly surprises and set you up for long-term success. A car is more than its sticker price. Monthly payments, insurance, maintenance, depreciation and future life changes all matter.

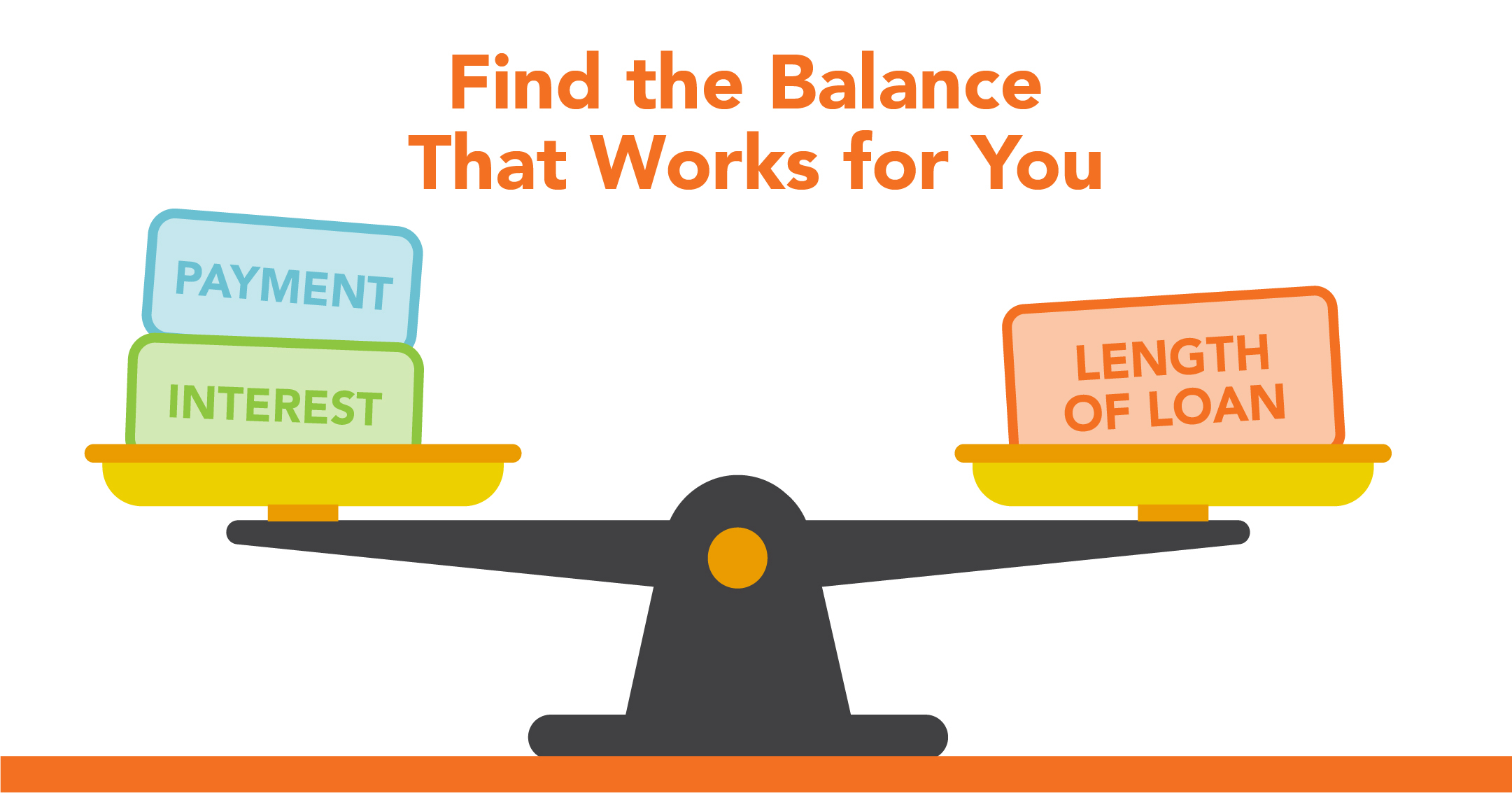

Before you start shopping, determine your budget and how long you want your payments to last.

If paying cash isn’t an option, getting pre-approved for a loan through your credit union is a smart first step. A pre-approval gives a clear picture of how much you may be able to borrow so you can shop with confidence and avoid shopping outside your price range. Down payment requirements vary by lender and depend on factors such as credit history, vehicle type, loan amount and LTV (loan-to-value). LTV compares the amount you’re borrowing to the vehicle’s actual market value. If the purchase price is higher than the value, you may need to make a larger down payment.

Auto loans typically range from 60 to 72 months, though terms can be shorter or longer. Longer terms may lower your monthly payment but increase the total interest paid. A down payment can help reduce both your payment and overall interest costs.

Leasing is another option. Leasing often offers lower monthly payments but does not provide ownership or equity. Leases typically include mileage limits, customization restrictions, and upfront costs, while a loan allows you to build equity that can be used for a trade-in or future down payment.

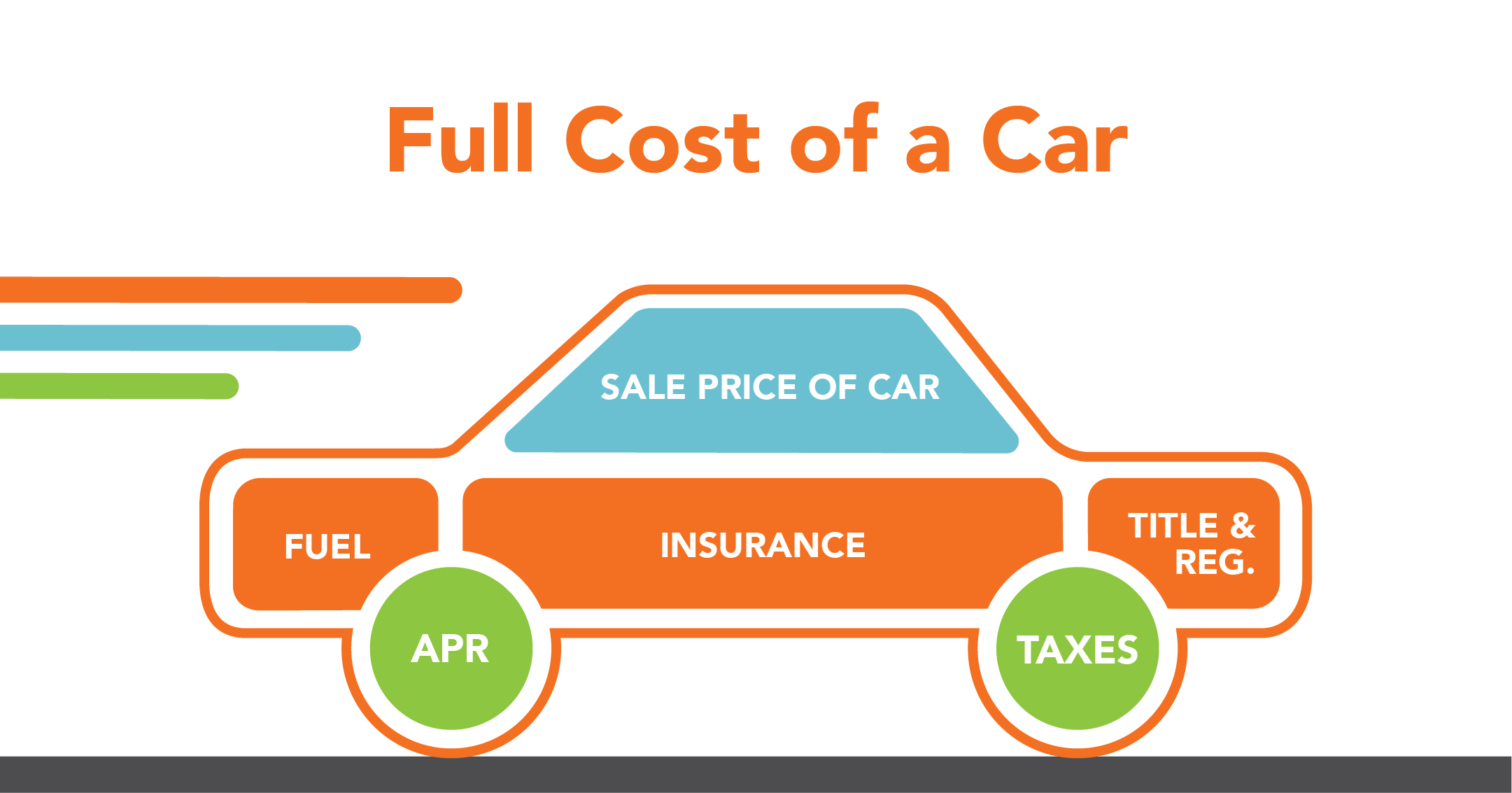

The loan payment is just one part of the picture. Be sure to account for additional costs such as the title, registration, taxes, and any additional options you may choose, such as a Route 66 Extended Warranty and other vehicle protections offered by Ascentra.

In addition:

- Fuel expenses can also add up, especially if you have a longer commute.

- If you are financing or leasing, insurance is required, including premiums and deductibles. To fully understand the cost of ownership, it’s important to request insurance quotes before buying.

- Maintenance and repairs are a key part of vehicle ownership. Routine services like oil changes, tires, and batteries add up, and unexpected repairs can happen. Planning ahead helps reduce stress.

- Consider how your life might change in the next five years, is the vehicle you’re considering big enough to grow into? Will it tow the boat or camper you hope to buy someday? We ask this because depreciation matters: many cars lose significant value early, and if you re-sell too early, you may owe more than the vehicle is worth, which is why used vehicles may offer better value.

Always go for a test drive, check for recalls, review vehicle history reports and watch for rebuilt or salvage titles. Taking time to research helps protect your investment.

Buying a vehicle is about more than transportation. It is about choosing something that fits your budget, lifestyle, and future. Ascentra Credit Union is here to guide you every step of the way so you can drive forward with confidence.

Before you head to the dealership, learn more about Ascentra's vehicle loan options or talk with our team to learn how we can help you establish a budget and get you pre-approved, giving you the confidence to be the negotiator.

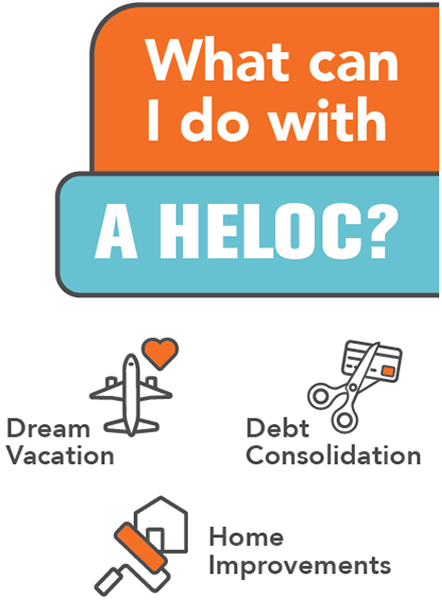

A Smarter Way to Borrow for Homeowners

During the early-to-mid stages of homeownership, many homeowners begin to accumulate equity in their homes. That equity isn’t just a number on paper; it can be a powerful financial tool. One of the most flexible ways to access it is through a Home Equity Line of Credit or HELOC from Ascentra Credit Union.

A HELOC works like a credit card backed by the value of your home. Instead of taking out a lump sum loan, you are approved for a credit limit, and you can borrow what you need when you need it. Interest is charged only on the amount you actually use, making it a more cost-effective and flexible option than many other types of borrowing.

So, why is a HELOC a better way to borrow money?

- Interest rates are typically lower than credit cards, personal loans, or even some auto loans because your home acts as collateral. This means a lower monthly payment and less interest over time.

- Repayment terms are flexible. During the draw period, usually 5 – 10 years, you can make interest-only payments or pay down the principal as your budget allows. Afterwards, you enter the repayment period, giving you predictable monthly payments over the remaining term.

- HELOCs are also ideal for specific life goals that many people face: home renovations, debt consolidation, education expenses or major family milestones. Unlike personal loans, which are fixed and can limit your options, a HELOC gives you access to funds whenever you need them, with the ability to borrow multiple times within your credit limit.

It’s important to borrow wisely but for those who plan wisely, a HELOC can provide financial flexibility, lower costs and peace of mind that comes with knowing you’re borrowing smartly. Ascentra is here to help. Before taking out your next loan, consider if a HELOC is a better way to borrow the money needed. Reach out to one of our dedicated Home Equity Specialists to learn how a HELOC may be a better way for you to borrow. Get started at ascentra.org/heloc.