Spot Predatory Lending and Use Smart Alternatives

It is the first of the month, your bank account is nearly empty, and rent is due. Desperate, you turn to a payday lender for a quick loan until payday. But then your car breaks down, and suddenly you are borrowing again, digging deeper into debt. This scenario plays out for millions of Americans every year. The good news? You can avoid turning a tough situation into a financial disaster.

How to recognize predatory financial services, understand how they operate and choose better solutions

Payday loans are a predatory pitfall

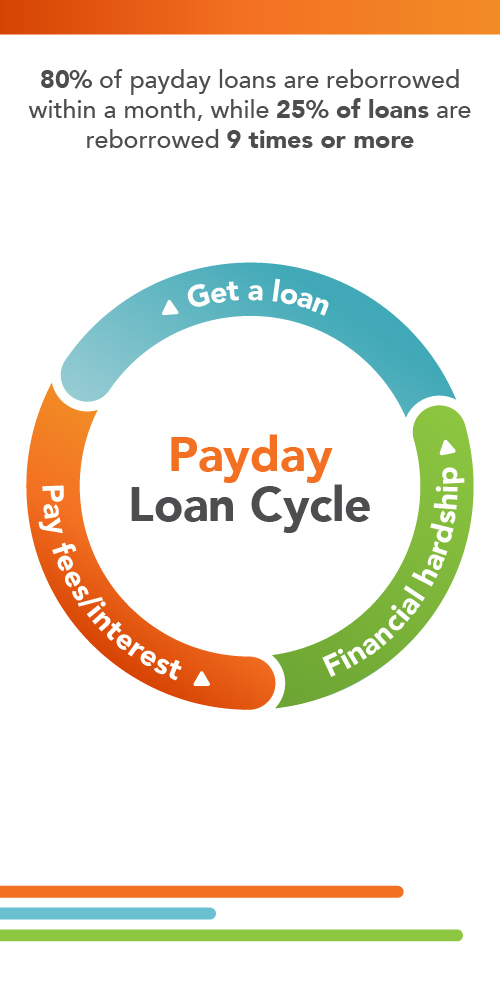

Payday loans, for example, are promoted as quick fixes, no credit checks, instant cash, but the reality is far harsher. With annual percentage rates (APRs) ranging from 300 to 800%, these short-term loans can quickly spiral out of control. According to the Consumer Financial Protection Bureau, over 80% of payday loans are reborrowed within a month, and one in four borrowers reborrow 9 or more times. Borrowers often end up paying more in fees than they initially borrowed.

Predatory lenders promise quick relief but keep borrowers trapped in cycles of debt

Payday lenders profit when customers are unable to repay their loans. They target people who may not have access to traditional financial institutions and often lure them in with additional services, such as check cashing, for hefty fees. Cashing a $1,000 paycheck could cost $50 or more each time, adding up to over $1,300 a year. By contrast, credit unions typically let members cash checks for free and offer the convenience of direct deposit.

Pawn shops are another predatory risk

Pawn shops offer quick loans against personal items like jewelry or electronics, but with high interest and short repayment windows, usually 30 to 90 days. If you cannot repay on time, they will either extend the loan for extra fees or sell your valuables. In a 2019 survey, 73% of pawn borrowers still owed money six months later.

Car title loans can leave you stranded

Car title loans are similar because they use your car as collateral. Title loan lenders rarely verify income or credit; they do not need to, because if you default, they take your car. Many own dealerships, meaning they profit from both your payments and the resale of your vehicle.

Rent-to-own stores may seem harmless but can be just as predatory

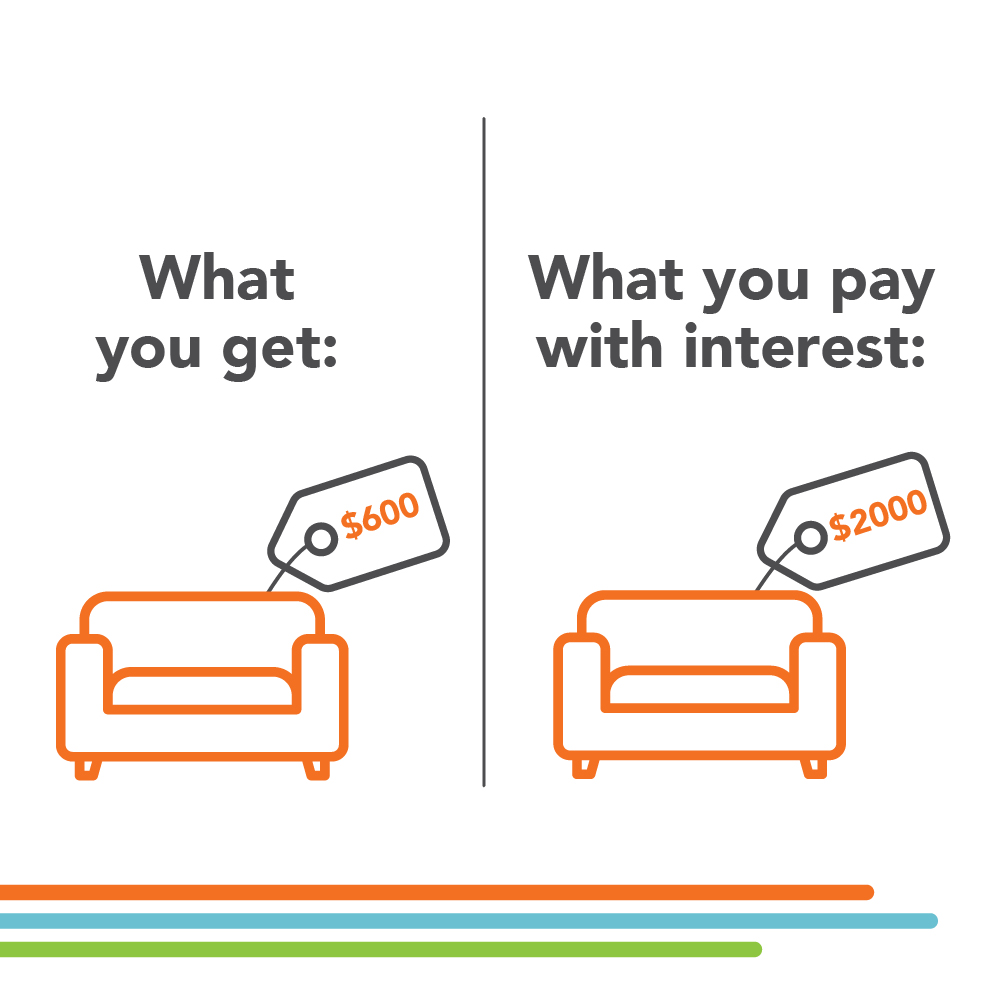

Paying $30 a week for a couch might sound affordable, until you realize that the same $600 couch could cost you $2,000 by the end of the contract. With effective APRs ranging from 43 to 468%, rent-to-own agreements charge far more than a traditional purchase or even a credit card.

Even housing can fall into the predatory trap

“Rent-to-own” or contract mortgages often target people who cannot qualify for traditional loans. These deals typically include high interest rates, balloon payments and strict terms. Miss a payment or break a rule, and you lose both the home and every dollar you have invested.

If you need emergency cash, a personal loan from a credit union is a far safer choice. You will get better rates, longer repayment periods and transparent terms. Credit unions, like Ascentra, even offer loans, such as “CashNOW” of up to $2,000 without a credit check. These loans are reported to credit bureaus, helping you build credit as you repay.

A credit union offers fair loans, financial coaching and long-term solutions to help you build stability and wealth. When money is tight, it is tempting to use the first lifeline offered, but not all lifelines lead to safety. Many are anchors that pull you deeper into debt. With the right financial partner and a solid plan, you can stay afloat, regain control and steer toward the financial future you deserve.

Personal Data: A Valuable Currency

In the modern internet age, personal data has emerged as one of the most valuable digital assets — a currency that funds connectivity. Consumers are often asked to provide their data to gain access to various convenient services. But these conveniences may come at the expense of the consumer’s privacy and security. This may include fraud, unwanted surveillance, identity theft and other scams that impact millions of people. Unfortunately, data collection is unavoidable, which makes data protection essential.

Here’s what you can do to protect your personal information:

Reduce Vulnerabilities

- Even though it’s nearly impossible to use various services without providing personal information, it’s important to think about potential vulnerabilities for what you share. For example, when using mobile applications, opt out of any unnecessary permissions; a flashlight app shouldn’t need access to your text messages.

Stay Alert for Scams

- Personal data often gets stolen when people fall for common scams both on and off the internet. You can avoid this by staying alert for warning signs, such as threatening or urgent language. Treat all requests for information with skepticism and never assume someone is who they claim to be.

Prioritize Privacy

- Cybercriminals are always looking for easy ways to gain access to someone’s personal information. Social media is one of their first stops because they know some people tend to share more than they should. Don’t make that mistake. Limit what information you make public and set social media accounts to private.

Use Strong Passwords

- Online accounts often have access to highly confidential information. Protect them with strong passwords that meet modern standards. A strong password is long and difficult to guess, avoids repeated characters and is unique to each account.

Remember: Security awareness is vital to protecting personal data, both at work and at home.